|

|

|

|

M&A Mastery Weekly

Insight and strategies for aspiring acquisition entrepreneurs |

|

|

|

Are you willing to do what the market requires to get a deal done?

Most buyers don’t lose deals because they are underqualified.

They lose them because they resist the realities of private capital.

This week, we’re digging into one of the biggest disconnects between aspiring buyers and actual owners:

Why personal guarantees are not some exotic trap, but a necessity of cash-flow-based lending in small business acquisitions.

And why trying to eliminate all risk before you act is one of the most common psychological mistakes that kills deals before they start.

➡️ Video: Is a Personal Guarantee Required to Buy a Business?

➡️ Article: 6 Common Mistakes Buyers Make That Kill Deals

➡️ Announcements: 3/12 Office Hours and The Women's Investor Survey (We'd Love Your Input)

Together, the video and article answer a broader question: Are you ready to compete in the real private market, or are you still trying to completely de-risk your acquisition?

P.S. If you know someone who says they want to buy a business but keeps looking for the “risk-free” version, forward this to them. |

|

|

|

|

|

|

|

|

Weekly Video

“Refusing a personal guarantee is refusing the market.”

Many buyers initially think a personal guarantee is a red flag, but it's not. It's a prerequisite.

If you’re using leverage to buy a business, a personal guarantee is simply how the private capital market works.

In this video, I break down why personal guarantees became standard in small business acquisitions, and:

-

Why SBA-backed lending unlocked deals under $10M and what lenders require

-

How banks, sellers, and buyers think about risk inside the capital stack

-

Why refusing to sign a personal guarantee dramatically shrinks your deal universe

If you want to compete for quality businesses, not just the leftovers, you need to understand this. Watch this before you structure your next offer. |

| WATCH THE VIDEO HERE |

|

|

|

|

|

Weekly Article

6 Common Mistakes Buyers Make That Kill Deals

After nearly two decades in this market, buying companies, brokering transactions, and watching hundreds of searchers move through the process…

I can usually tell within five minutes whether a buyer will ever close.

It doesn’t have anything to do with their resume (or buyer profile as we help you create in the Lab), how many books they’ve read (even mine), or how knowledgeable they appear on a call.

It shows up to what extent they’re prepared: the questions they ask, whether they’re pre-qualified, their relationship with risk, and if they’re finally ready to take the leap.

First-time buyers think deals fall apart in diligence, but they usually do before an offer is ever submitted – the buyer has already disqualified themselves without realizing it.

Here are the most common ways buyers do that.

1. Not Getting Pre-Qualified

If you were buying a house, no real estate agent is going to take you to see a $1.5 million home without a pre-qualification letter. That just doesn’t happen.

Buying a business is no different.

Buyers start looking at deals without knowing if they can get financing for one.

Ten people say they are serious. Maybe two of them have actually talked to a lender and gotten pre-qualified.

|

|

|

I can’t take you to meet my $1.5 million seller if you can’t demonstrate access to capital because the first question every seller asks is, “Do you have money?”

The first question every broker asks is, “Do you have access to money?”

As a broker, if the answer is vague, I immediately move down the priority list.

Traditional search funds understood this decades ago. They may not have committed capital at the beginning, but they can point to multiple backers. That credibility is one reason their average deal size is often ten to fifteen million.

You don’t need all the money in your checking account, but you need a viable path to it. Without access to financing, you’re not buying – you’re window shopping.

2. Trying to Completely De-Risk the Acquisition

Buying businesses is as much a psychological game as it is a financial one, and this mistake is one of the most common psychological ones.

Buyers try to eliminate all risk before they act.

The truth is, you can’t fully de-risk a business. There will be customer concentration, seasonality, cash flow gaps, key-person dependency, regulatory shifts, employee turnover, cultural friction, and more.

The question is not whether risk exists. The question is whether you understand the risks well enough to take a calculated bet.

Are there “safe” businesses with recurring revenue, high barriers to entry, healthy cash flow, and management team fully in place?

Sure. But when those businesses come to market, you will never see them because they will sell instantly.

With the “perfect business” off the table, the focus is less on eliminating risk and more on aligning your value with the right business.

|

|

|

What do I bring to the table?

What is my attitude?

What is my aptitude?

What action am I willing to take?

If you find yourself unable to make the leap from analysis to ownership, you might be trying to play it too safe.

3. Buying a Job, Not a Business

I have seen countless businesses that looked great on paper, with decades of revenue and strong margins, but one person was doing it all. It’s really incredible how far a single business owner can take a business.

However, just because a business has great top-line revenue doesn’t mean it’s transferable.

If all the relationships and specialized knowledge live in the owner’s head, you are not buying a machine. You are buying a human.

You need to ask yourself, can this operate without the current owner?

If the answer is no, either the price must reflect that reality or you must be prepared to build the infrastructure yourself.

|

|

4. Over-Indexing on Why the Seller Is Selling

I once bought a distribution business that looked risky on paper, with customer concentration and soft revenue, because I discovered the business was more sound than it initially appeared.

Turns out, the owner was the bottleneck, and fixing the leadership unlocked value.

This is why I always say, figuring out why the seller is selling is important, but it’s not everything.

Buyers listen for the words burnout, financial distress, divorce to try to uncover some hidden disaster.

Sometimes there is one, but often there is not.

The deeper question is whether there is an unresolved structural issue or whether there is untapped potential.

If you stop at surface level suspicion, you may miss a great deal.

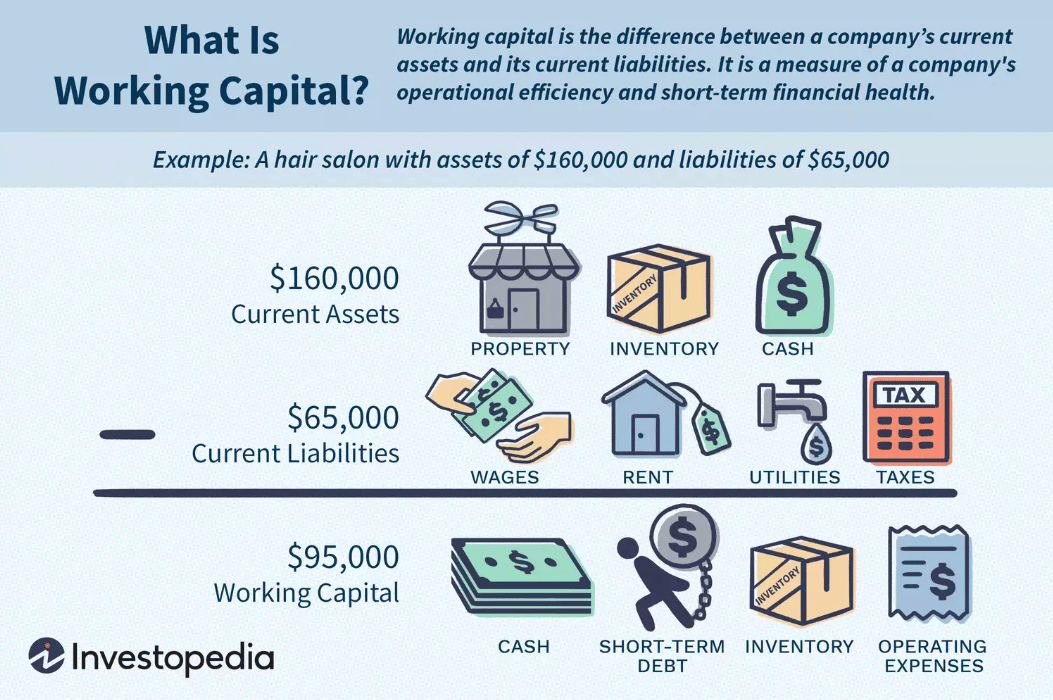

5. Mishandling Inventory and Working Capital

One of the biggest mistakes during diligence is that buyers assume they have to take all the inventory that’s on the balance sheet, even if it’s years old. You don’t.

If that inventory will not convert to cash in the first ninety days, you don’t want it.

Sometimes the right move is to require the seller to liquidate excess inventory before closing. You don’t want to let accounting games manipulate the perceived value of the company.

Working capital should reflect operational reality, not wishful thinking.

|

|

|

Source: Working Capital | Investopedia

6. Not Having Financing When Submitting Offer

Here is another common scenario.

The broker asks whether you have the ten to twenty percent down payment. You say you can probably raise it.

If there’s no one else interested in the listing, you might have a chance.

But if there are four qualified buyers and you are the only one who still needs to assemble capital, you are not in a strong position.

Here’s why: Sellers care about certainty more than they care about price.

A seller would often rather take a slightly lower offer from a buyer who is fully capitalized than a higher offer from someone who still needs to “line things up.”

Not only do deals fall apart in financing, but financing also takes time. From the seller’s seat, that means months of exclusivity with a buyer who may not close.

And every month under LOI is a month their business is in limbo. Employees get nervous, customers sense distraction, and momentum slows.

So brokers screen for this early.

This is why being pre-qualified and having equity lined up is not a formality, it’s competitive positioning.

It Comes Down to Buyer Readiness

Most acquisition mistakes are not technical – they are structural or psychological.

Sellers are asking one simple question: Are you ready?

If you can answer that question with capital, conviction, and clarity, you move from dreaming about buying a business to actually owning one.

Ready to acquire a business in the next 12 months? The Acquisition Lab is your first stop. Reach out to us today and get on the fast track to becoming an acquisition entrepreneur.

|

|

|

|

Upcoming Webinar

Office Hours: How to Manage the Transition

When you close on a business, the real work isn't growth or staff changes.

It starts with the transition first.

In this upcoming Office Hours session on 3/12 at 12 pm ET, we’re breaking down what transition actually looks like in the first days after closing.

Not theory, but the real mechanics.

You’ll hear firsthand lessons from Lab members on:

-

Opening new bank accounts and payment processors

-

Transferring merchant services and phone systems

-

Moving registrations, utilities, and insurance into your name

-

Setting up payroll and employee benefits

-

Gaining control of systems, passwords, vendors, and subscriptions

These are the operational details that protect stability, and they’re rarely taught.

We’ll talk about what surprised them, what went smoothly, what created friction, and what they would plan differently next time.

Getting your transition right from the beginning sets the tone for everything that follows.

|

| REGISTER NOW |

|

|

|

Investor Survey

The Largest Untapped Capital Pool

Women control a rapidly growing share of global investable assets.

Yet participation in private markets — private equity, private credit, direct business ownership — remains disproportionately low.

That gap isn’t about competence. It’s about access, networks, and how opportunity is structured.

In partnership with The Investor Collective, we’re launching the Women’s Investor Study, a research initiative designed to better understand how women are thinking about private investing today.

What’s working?

What’s missing?

What would increase participation?

If private markets are where asymmetric wealth is built, then understanding this capital shift matters.

Whether you’re actively allocating to private deals or just beginning to explore them, your input will help shape how the industry understands and serves women.

If you’re allocating capital or considering it, we’d value your perspective. Please take a few minutes to share it.

|

| TAKE SURVEY |

|

|

|

|

|

|

If you want to buy a cash-flowing business and avoid common mistakes first-time buyers make, Acquisition Lab is for you. We offer world-class education and access to a vetted community of acquisition entrepreneurs.

Apply below to enroll now! |

|

|

|

|

|

|

|

|

|

|